Should I Be an LLC, Sole Proprietor or S Corp?

You may be just starting a business, or maybe you are a freelancer with an existing business where you are a sole proprietor. Maybe you want to expand your business and add more partners and are considering incorporating for the first time into a business entity. You might have a packed and full day already, but are performing some side work on a startup, hoping to turn it into a full-time real business. If you are ready to take the next steps into entrepreneurship, the first step you will want to take is establishing a legal business entity. This is not as easy as it may sound because there are a lot of moving parts in the selection of the right business entity for your purposes. Ideally, you will want the entity structure which will protect your personal assets from any liability you may incur as a business owner, while also offering you some substantial tax advantages.

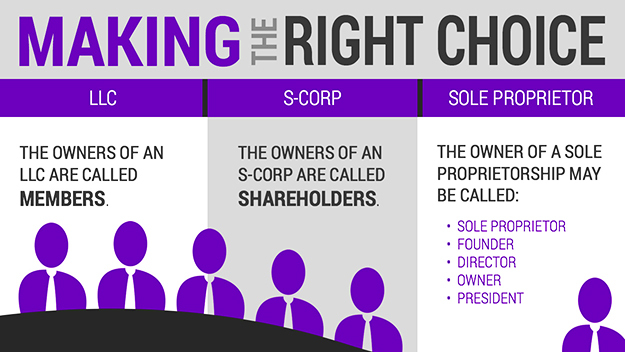

Again this sounds easy enough to do, right? Probooks NY is very familiar with this process and has witnessed the intricacies and complications that startup business owners face as they move to formalize their startup’s activities, as they relate to structuring a new entity. Entity selection is a crucial process and needs to be extensively researched and thought about thoroughly. When you begin to organize your company, don’t be surprised if it’s a little confusing given that each entity option has its own tax and legal benefits. Note that the three most commonly used business structures for self-employed startups are sole proprietorships, limited liability corporations (LLC), and S corporations (S corp).

Here is a brief explanation of these entity types and both the advantages and disadvantages that each can offer with regards to taxation.

Sole Proprietorship Entity

If a startup entrepreneur chooses no particular business form, he will operate his business as a sole proprietorship. This is the simplest of all forms and generally requires nothing more than a certificate of an assumed name, in the event the owner decides to name the company. The downfall here is that, if you choose to go with being a sole proprietor, then you will not have any protection against personal liability that may be incurred as a result of your business activities. Sole proprietorships offer nothing in terms of limited liability. If you, as the owner, or an employee commits a tort, you can be sued personally.

The “no limited liability factor” should be an important consideration; this is especially true if you are planning to transition into a full-time freelancer (graphic designer, writer, videographer etc). Simply put, you will now have significantly more exposure than if you were working part time. If looked at from the tax perspective, a sole proprietorship is like a single member LLC, which does allow a more streamlined approach to tax filing. The reason being is that the IRS considers a sole proprietorship as a “disregarded entity”, which means, that your income from your business is reported on your personal tax return (Form 1040), instead of on a separate business return.

LLC Entity

LLCs have gained popularity as a relatively simple vehicle for achieving limited liability and flexible tax treatment, without the onerous paperwork requirements associated with starting and operating a corporation. A single member LLC offers a major legal advantage by protecting your personal assets from the creditors of your business. And, by setting up an LLC, you also can avoid paying both personal and business taxes on your income. As a “pass-through entity” all of the income and expenses from your LLC get reported on your personal income tax return because you are the business operator. Regardless, you will have an operating agreement whether you create your LLC as a single or multi-person company. If you have a few partners, you need to be more careful to spell out each others’ rights in the event of a split up, death or irreconcilable disagreement.

A single member LLC is easier for tax purposes because no federal return is required unless the business decides to be treated as a corporation for tax purposes. Income is reported on each member’s personal tax return. A multi-partner LLC must file tax returns, and provide its members with K-1 forms. The K-1 form breaks down each member’s share of the LLC’s profits and losses. In turn, each LLC member reports this profit and loss information on his or her individual Form 1040 returns, with Schedule E attached.

S Corporation Entity

The S corp is a popular choice for many startup businesses. An S corp, similar to an LLC, does give you personal protection from any business liabilities you may incur from a financial perspective. Establishing an S corp also helps you avoid paying both personal and corporate taxes. A major difference between S corps and LLCs is that S corps pay themselves their salaries and receive dividends from any additional profits the business may earn. This adds another dimension of complexity to the tax situation because of the required tax regulations that S corp owners must comply with. Another thing to point out is that S corp owners must file business tax returns, rather than just using their personal tax returns to report their business income. Also similar to an LLC though, S Corps offer the option for their shareholders to avoid double taxation by receiving pass-through tax treatment, where the corporate profits are passed through to the individual shareholder returns. An S corp isn’t a particular type of entity itself, but rather a corporation that has elected tax treatment under Subchapter S of the Internal Revenue Code. As a corporation, it requires the appointment of a board of directors and the holding of annual shareholder meetings.

Another thing you should know is that under each entity scenario, you are allowed pre-tax expenses, such as office equipment, travel, advertising, promotion, car expenses and even health care premiums. If you work from home sometimes you may be able to deduct a home office expense.

What is Better for Tax Purposes?

Let’s take a closer look at the tax implications or consequences of establishing an LLC vs. S corp- the two more commonly used types of entities that startups and self-employed small business owners might establish. Entity choice depends on what type of business you have and how far you are looking to grow it. Both entities have pros and cons depending on the scenarios; a case-by-case approach should be taken.

When might an LLC be better?

There is less red tape and less expensive formation and administrative fees to set up an LLC than an S corp. So, if you are a small business owner or running an internet eCommerce company then an LLC might be your better option. But, say your eCommerce startup is growing in revenue and you begin to get shocked by how much you are paying in taxes. It’s highly recommended that you consult your CPA, who will likely tell you that there is a way to be taxed like an S corp while keeping your LLC intact. Assuming you take this advice to become an S corp, you need to do a massive overall of your salary structure and begin paying yourself a more modest salary; your salary should also include fees like FICA and unemployment insurance. You may wonder how you can determine the dollar figure that coincides with a modest salary. IRS suggestions are vague in this area and only stipulate that S-corp salaries be realistic. In essence, you should definitely pay yourself a little more than minimum wage. This may seem extreme but you have to remember that extensive dividends (assuming your business is successful, so to speak) will be coming your way as a result of your S corp’s election to see income flow through in the form of dividend payments. This entity arrangement could amount to thousands in federal tax savings! In this scenario you get the best of both worlds: you can run your business as an LLC, but get taxed as a S Corp, which is quite desirable if your revenue is growing. However, the tax rate for an LLC depends on the total income of the owners. At higher levels of net income, the LLC may be paying taxes at a lower tax rate than an S corp.

When might an S corp be better?

While the small business scenario we just mentioned is interesting, if you have a fast-growing startup businesses you may want to change your strategy. If you are expanding as a business and planning to raise capital by bringing on investors or sharing ownership of the company with your employees, then you may need to consider making the switch to an S corp sooner than later; this is especially true once you exceed $500,000 in annual revenue. If you run your idea by your CPA , you will want to know some of the disadvantages of operating as an S-corp. The downsides are evident in that there is more paperwork to file to substantiate your request. You also are required you to hold meetings, keep minutes, make resolutions, elect officers and produce formal financial statements. The S corp structure creates more separation between you and your company and gives bankers and investors a certain confidence if they are planning to invest.

Making a Decision

Choosing a new type of business entity is best accomplished after consultation with a lawyer and a CPA. A sole proprietorship may be the best choice for a sole-member startup with no employees, as members and shareholders are always personally liable for their own errors… limited liability offers no advantage if there is no one else to sue. An LLC makes more sense for a business that may hire employees in the future. An S corp may provide the best option if the ultimate goal for your venture is to sell it. Pro Books NY offers small business consulting services. Contact us for a consultation.