The idea of sales tax was created during the times of the great depression. Then, during the mid-1930s, 24 states and the District of Columbia began enacting and imposing a sales tax. As of 2017, we have 45 states that use sales tax for revenue. The five states that currently remain sales tax-free are Alaska, Delaware, Montana, New Hampshire and Oregon. There is a caveat though…many local municipalities in those states often impose surcharges on businesses.

The idea of sales tax was created during the times of the great depression. Then, during the mid-1930s, 24 states and the District of Columbia began enacting and imposing a sales tax. As of 2017, we have 45 states that use sales tax for revenue. The five states that currently remain sales tax-free are Alaska, Delaware, Montana, New Hampshire and Oregon. There is a caveat though…many local municipalities in those states often impose surcharges on businesses.

The complexities of state sales tax can cause a lot of issues, especially for e-commerce small business owners. This system, if it is not understood, can create extra costs and fees for a business, whether they are doing commerce in one or multiple states.

To review the basics of how state sales tax is intended to work is that every business needs to file and remit sales taxes for any state it has a presence in. Following that, the owner, or the business’ respective accounting firm, need to determine the tax rates at the local and state level. Tax rates vary based upon the item sold and the location of the business or the customer.

It sounds relatively simple– but it’s anything besides easy. Before the advent of e-commerce, physical presence in a state was fairly straightforward. But the rise of online retail — dominated by Amazon and its extensive affiliate network — has prompted states to find new ways to collect sales and income taxes from companies that conduct business virtually online. Amazon now pays sales tax in 19 states, though it has long argued it has a physical presence in only a few of them.

Here are four important questions that every small business owner should ask and ultimately find out they navigate the complexities of state and local sales tax.

The following are three key questions every small business owner should ask as they start navigating the complexities of sales tax.

1. How does my state actually define my business’s physical presence?

For a local jurisdiction or state to require a business to file and remit sales tax, the said business must have a sufficient physical presence, or “nexus.” which also means having “a connection or tie”. Now, the definition of a physical presence is somewhat loosely defined and can vary depending on the state, but at the basic level, it is whether there is a temporary or permanent presence established. Employing independent sales reps within a state may also qualify as a nexus.

Some states consider a seller to have sales tax nexus in the state if you have any of the following in the state:

- An office or place of business

- An employee present in the state for more than 2 days per year

- Goods in a warehouse

- Ownership of real or personal property

- Delivery of merchandise in Arizona in vehicles owned by the taxpayer

- Independent contractors or other representatives in Arizona for more than two days per year

2. How does my state tax my specific products or services?

Sales tax rates can differ based on the type of products or services sold. As an example, prepared food may be subject to sales tax in one state but not in another. The same applies to various types of clothing, groceries, prescription drugs and other items or goods for sales.

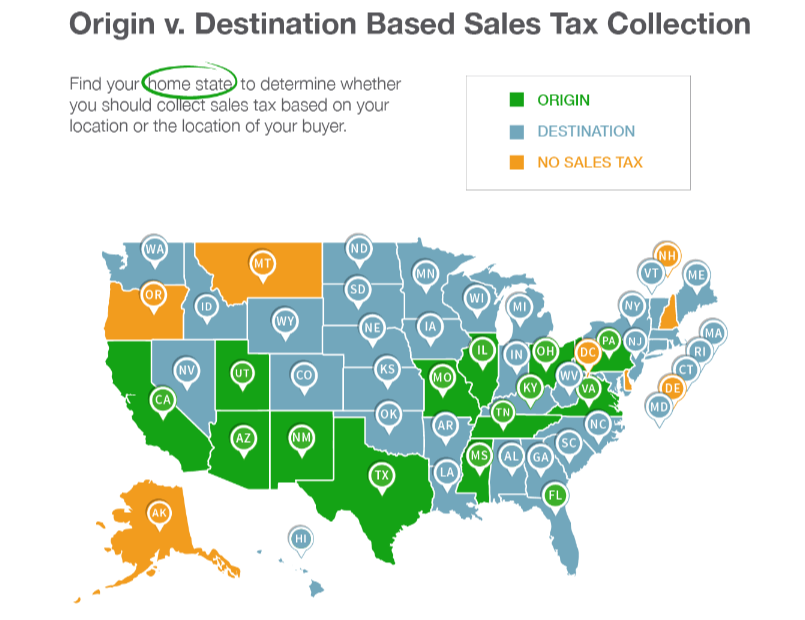

3. Is my state sales tax based on the location of my business or my buyer?

When it comes to charging sales tax, online sellers need to know one key fact: whether you are based in an origin-based sales tax state or a destination-based sales tax state. This is key to knowing how much sales tax you should charge your customers. And it can get confusing!

In destination-based states, companies charge its customers’ sales tax based on the location where the items are being sent.

List of Destination-Based Sales Tax States

And with destination-based taxes, businesses are responsible for tracking and reconciling different state and local taxes. As an example, If the destination’s state tax rate is four percent, but the business is delivering it to a customer in a city with a local tax rate of four percent, the business must charge a total-sales tax of eight percent. As of 2017, the following states use destination-based taxes:

- Alabama

- Arkansas

- Colorado

- Connecticut

- District of Columbia

- Florida

- Georgia

- Hawaii

- Idaho

- Indiana

- Kansas

- Kentucky

- Louisiana

- Maine

- Maryland

- Massachusetts

- Michigan

- Minnesota

- Nebraska

- Nevada

- New Jersey

- New York

- North Carolina

- North Dakota

- Oklahoma

- Rhode Island

- South Carolina

- South Dakota

- Vermont

- Washington

- West Virginia

- Wisconsin

- Wyoming.

List of Origin-Based Sales Tax States

States with origin-based laws, tax customers based on the location of the business as opposed to that of the customer. That rate could include a combination of state, county, city and district tax rates. For example, if the company resides in a state with a five percent sales tax rate, all customers are going to be taxed at a rate of five percent no matter where in the country they are located. As of 2017, the following states use origin based taxes:

- Arizona

- California*

- Illinois

- Mississippi

- Missouri

- New Mexico

- Ohio

- Pennsylvania

- Tennessee

- Texas

- Utah

- Virginia

* California is unique. It’s a modified origin state where state, county and city taxes are based on the origin, but district taxes are based on the destination (the buyer).

4. What are the rules if you have sales tax nexus in more than one state?

If you have sales tax nexus in multiple states, there’s more to the story.

States have a whole different set of rules when it comes to “remote sellers.” A state considers you a remote seller if you have sales tax nexus in that state but are not based there. (In a state’s terminology, this is called “use tax.” But “use tax” is basically the same thing as sales tax, only as applied to remote-sellers.) For example, if you sell via Amazon FBA (Fulfillment by Amazon) and live in Georgia, but your products are shipped to a warehouse in Tennessee, Tennessee would consider you a remote seller. If you were based in Tennessee, you would charge sales tax based on the rate at your business’s location, because Tennessee is an origin-based sales tax state. But Tennessee is actually a destination-based sales tax state when it comes to remote sellers. So if your business is based in Georgia but have sales tax nexus in Tennessee you would do one of two things:

1.) Charge sales tax at the rate of your buyer’s ship to location

2.) Charge a flat 9.25%

Conclusion

To say the least, figuring this out and satisfying all the sales tax laws requirements can be a confusing, time-consuming process. This blog is for informational purposes only. Be advised that sales tax rules and laws are subject to change at any time. For sales tax advice and guidelines specific to your business, be sure to contact Probooks NY for a consultation.